Can we avoid ABSD?

Can ABSD be avoided?

The answer is both Yes and No as it is depend on case by case basis…

What is ABSD?

ABSD is based on the property count and nationality of the owner who attracts the higher stamp duty.

Exception for married couple who are buying their 1st Matrimonial Property & 1 of them is a Singapore Citizen.

There are several ways to hold the property…

Home Ownership Structuring

- Decoupling

- Manner of Holding

- 99/1

- Gift

- Trust

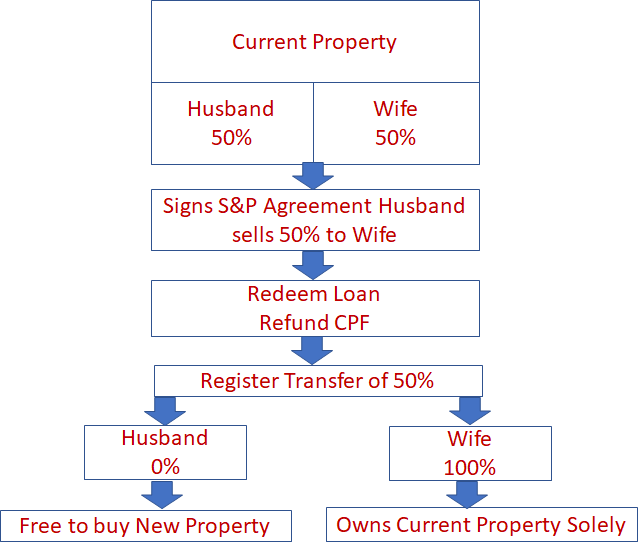

What is Decoupling?

The Sales & Purchase of all the share in a property of one co-owner to another co-owner of the same property so that only one owner owns the property.

This allows the outgoing owner to purchase another residential property without paying ABSD or paying a lower rate of ABSD.

Does HDB flats allow decoupling?

Decoupling has been disallowed since April 2016.

Case by case basis for parents & children, medical reasons, death, financial hardship, divorce or renunciation of Singapore citizenship.

How to we Decouple?

When can we buy the next property after Decoupling?

After the S&P Agreement for the Sale and Purchase of the 50% share in Current Property is signed & stamped.

Then can proceed to exercise the Option for the Purchase of the New Property.

Using CPF Refund of Decoupled Property to Pay Purchase Price of the New Property

If CPF Refund from Current Property is required to purchase the new property, the completion date of the new property must be 3 weeks after the completion date of the current property.

Considerations

So, what are the considerations?

- Is it worth it?

- Loan eligibility

- CPF Refund

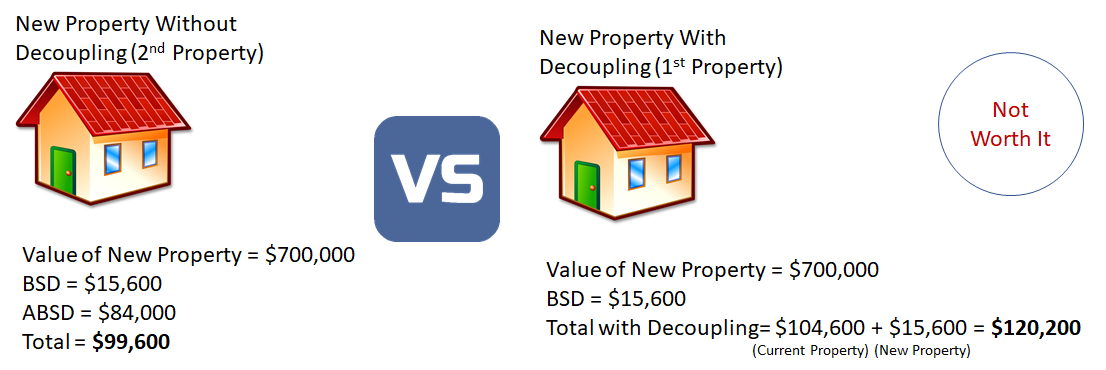

Is it Worth it?

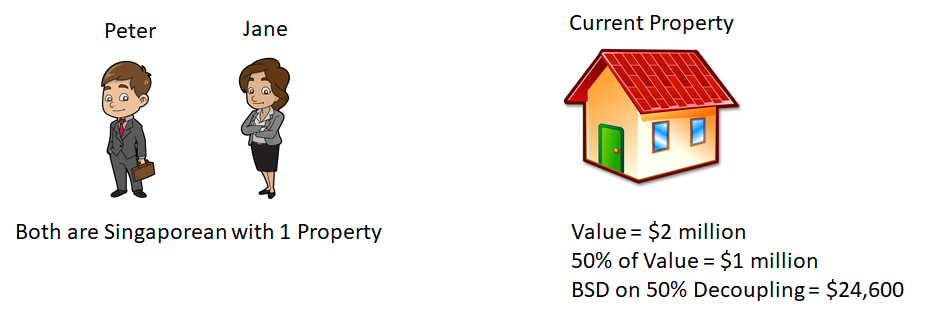

Let’s do some calculation.

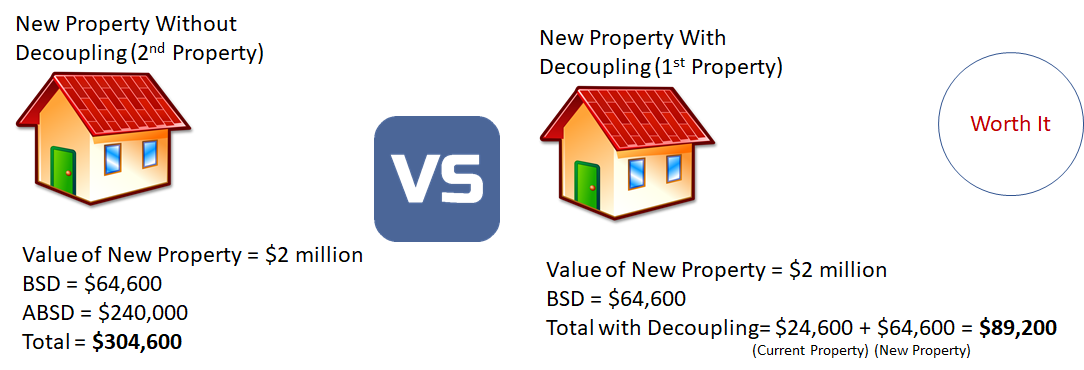

Clearly for this example its worth it to do the Decoupling as the total amount spend on decoupling is much lesser than the one without.

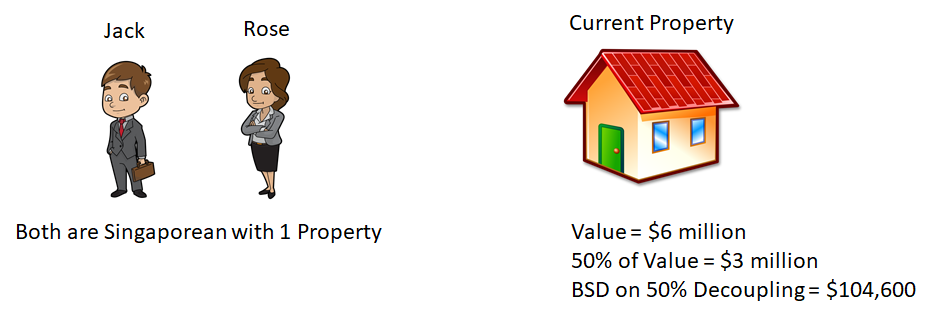

Now let's look at another example…

As you can see that the amount spent on Decoupling is more than without so its not worth it!

Loan Eligibility

Next we should also consider for the loan eligibility

Is Staying Owner (“Buyer”) able to maintain the existing loan in own name?

If yes then you may proceed.

If No, then original outgoing owner (“seller”) to remain as owner.

Or original Staying owner to buy a smaller new property.

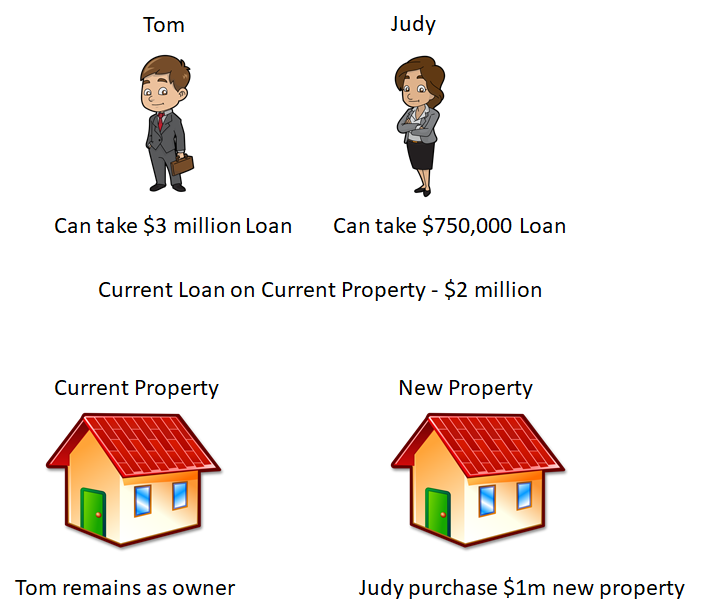

Now let us take a look at the example below

Recommendation

Judy sells her 50% share of current property to Tom

Tom remains as owner of current property

Judy purchases New property worth up to $1 million.

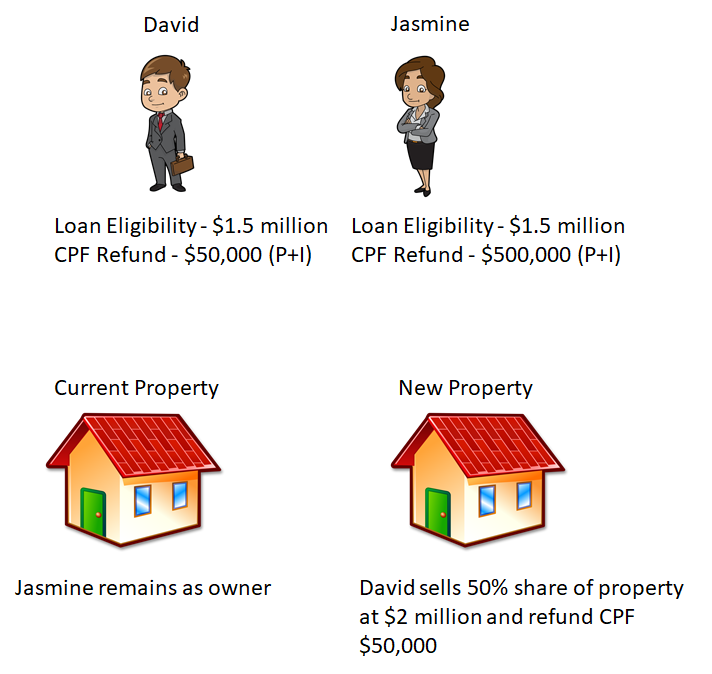

CPF Refund

Next we should consider the CPF refund

Can seller refund his CPF (P+I) ?

Recommendation

David sells his 50% share to Jasmine as her CPF refund is more.

David refund less of his CPF.

Now that we know what can or cannot be done, let us take a look at one case study..

Case study: 1

Married Couple

- Mr Lee is a Singapore Citizen with no property.

- Mrs Lee is a Foreigner with no property in Singapore.

1st Property: 99/1 shareholding

Mr Lee -1%

Mrs Lee (foreigner) – 99%

Stamp duty is based on Mr Lee’s nationality as he is a Singapore Citizen & married to Mrs Lee.

BSD – YES

ABSD – NO

They then do a Decoupling

Mr Lee sells his 1% share to Mrs Lee

Mr Lee – (SSD applies if within 3 years on the 1%)

Mrs Lee – (pays BSD + ABSD on 1%)

Mr Lee free to buy a 2nd property while Mrs Lee owns the 1st property

Side note that Mrs Lee must be able to take a loan on her name for the 1st property and Mr Lee must be able to refund is CPF(P+I).

Refund of ABSD

Only applicable to co-purchase by a married couple involving at least one Singapore Citizen spouse may apply for ABSD refund if:

- ABSD has been paid on the 2nd residential property

- 2nd residential property is purchased in joint names

- The 1st property ( co-owned or owned separately) is sold within 6 months from the date of the purchase of the 2nd property (if completed property) or TOP/CSC (whichever is earlier) of the 2nd property (if it is an uncompleted property)

- The married couple has not purchased or acquired a 3rd or subsequent property from the date of purchase of 2nd property to the date of sale of the 1st property.

- Application must be made within 6 months after the date of the sale of the 1st residential property.

- No change of ownership in the 2nd residential property at the date or disposal of the 1st residential property

- They remain married to each other.

Note: Covid-19 – Temporary Relief Measures for Property Sector

6 months extension for buyers selling 1st Residential property

- 2nd residential property is jointly purchased on or before 1 June 2020

- Original timeline to sell 1st Residential property expired on or after 1 February 2020.

Issues Arising from Decoupling

Manner of holding

Joint Tenancy

- Equal shares (50%/50%)

- Right of survivorship (cannot “will” the share)

- Must deal with property jointly

Tenancy-in-common

- Equal or unequal shares (50%-50% / 99%-1%)

- No right of survivorship (can “will” the share)

- May dispose of share without agreement of other tenant-in-common

After Decoupling

Documents to consider are

- Will

- LPA

- Agreement

Decoupling or not for 50/50 and 99/1?

50% & 50% | 99% & 1% |

| Loan Structure | Loan Structure |

1)75% of Purchase Price of 50% share 2)50% of outstanding loan | 1)75% of purchase price of 1% share or $0 loan 2)99% of outstanding loan |

| Suitable if intending outgoing owner used substantial of CPF | Suitable if intending outgoing owner didn’t use much CPF |

Read more on..

Should You Sell Your HDB Now ? - 2021

Why Sell Private Home Now ? -2021

What should homeowners buy after selling their HDB or Private Homes?